- Corn 2 ¾ to 1 lower

- Soybeans ¼ to 1 lower

- Wheat 5 ¾ to 7 lower

- Basis Flat

- Live Cattle 433 higher (238.35)

- Lean Hogs 97.08 +133

- Dow Jones 322 higher (49,186)

- Crude Oil 13 higher (74.69)

As the news out of Iran and the Middle East slowed today so did the volatility in all the markets with the equity markets showing the largest gains while the other raw material and commodity markets welcomed the far less volatile environment. While crude oil traded quietly on both sides of unchanged and finished modestly higher, whichever direction the energy markets go next will be followed by bean oil and ethanol and pull corn and beans in that same direction. With confidence in the mid-March trade summit in Paris and then the big meeting in Beijing, the market is optimistic China and the US will iron out an improved trade agreement in the next month. Thursday’s export report is expected to be solid for corn but just average for beans and wheat.

News and Notes:

- The combination of Argentina’s corn harvesting and Brazil’s corn planting and early development will need seasonal weather foe the next 8-weeks. The forecast looks good so far, but safrinha pollination forecasts will be closely watched. Rain continues to be teased for the driest areas of IL and IN the rest of the week. Soil moisture levels in N IL are worse than last year. Above normal temperatures and the possibility of an early spring for the Delta and SW will speed planting along in the month ahead. Weather will be a much bigger part of the conversation if the situation in Iran begins to be less volatile.

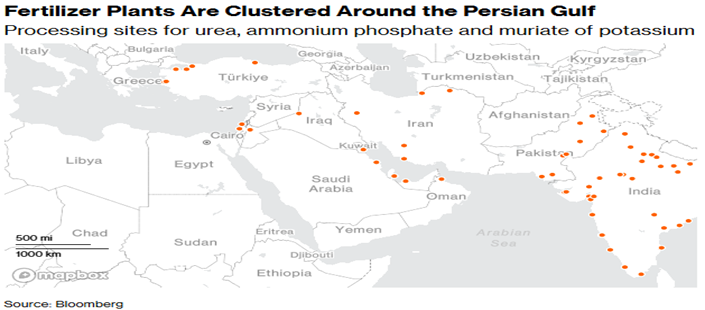

- The map on Page 2 shows the sites of the fertilizer plants in and around the Persian Gulf. The concern for everyone is that the war could spread across the Middle East or the Straits could be closed for anything else but crude oil tankers. With so much of the world’s commerce in energy and fertilizer products going through the Straits, whether it is coming to or from the US, prices will go higher which will go across the globe, not just the regions affected. It is important and timely that the US has a signed trade deal with India and a good relationship since India has 29 plants. Specific fertilizer imports were not highlighted in the trade deal, but our relationship with India is better than many other countries highlighted on this map.

- Diesel is now $1.30 over the 2025 close but Tuesday’s sharp early rally and deep pullback could be the top in diesel for now. When President Trump announced US war ships would escort oil tankers through the Gulf of Hormuz, the selling intensified. At this week’s high the trade was pricing in an extended closure of the Straits on panic buying, but a quick resolution to the closure and ending the aggressive strikes on Iran (or Iran surrendering), a sizable downside in diesel is present. Sunday night’s low at $2.61 is the first target to the downside. Today’s close was $2.cv. Be patient topping off your fuel tanks.

- After the weekend developments in Iran and China’s quick condemnation of the US attack, it was feared the April meeting between Xi and Trump might be cancelled. Both sides announced today that the highest-level trade representatives of both countries will meet in Paris in mid-March. Treasury Sec Bessent will attend which gave the soy and grain markets optimism that further Chinese purchases will be negotiated. If the war in Iran ends soon, the trade meeting will move to the top of the headlines.

- Corn exports have been above expectations for the first half of the USDA’s fiscal year. Over the last week there have been three small 8 MBU sales (4 cargoes) to Unknown Destinations, which almost always means China. All the trade meeting talk with China has surrounded buying more beans, but an active buying pattern from China would add more fuel to the corn rally. China typically does not buy a huge amount of US corn, but if an extra 400-500 MBU could be included in the bean purchases, the market bulls would notice.

- Although cattle rallied sharply today (now $12 off Monday’s low) an interesting side effect of the war could be Brazil losing their Middle East and Chinese beef export capacity. This could potentially push those exports to the US where beef and cattle prices remain near record high.

Is this the end of the storm or are the markets in the eye before the second wave of the hurricane? It appears the worst-case scenarios that were rocking the markets Monday and Tuesday have been scaled back but the tension and turmoil in the Middle East is far from over. Crude oil prices will be the best indicator of where corn and bean prices go until the conflict ends.

Sales Targets

Corn

Beans

Wheat

- 2024 Crop Finished Finished Finished

- 100% Sold at $4.46 Avg 100% Sold at $11.13 Avg 100% Sold at $6.20 Avg

- 2025 Crop 10% at $4.55- March '26 Finished Finished

- 80% Sold at $4.44 Avg 100% Sold at $10.67 100% Sold at $6.24 Avg

- Current Price $4.44

- 2026 Crop 10% at $4.85 - Dec ‘26 On Hold– Nov '26 On Hold– July ‘26

- 40% Sold at $4.70 55% Sold at $11.01 50% Sold at $6.13

- Current Price $4.70 $11.31 $5.78

%’s are total of expected yields. Bold Prices are Updated Sales Targets. * price includes trading

Today’s Market Closes — Rounded to the Nearest Cent

Corn

- May $4.44

- July $4.54

- September $4.56

- December $4.70

Beans

- May $11.70

- July $11.83

- September $11.36

- November $11.31

Wheat

- May $5.68

- July $5.78

- September $5.90

- December $6.07

Other Closes

- Apr Diesel 3.2781 +912

- US Dollar 98.430 -276

- Cash Cattle $248 Offer

- Feeder Cattle 363.93 +673

Any decision to purchase or sell as a result of the opinions expressed in this report will be the full responsibility of the person authorizing such transaction. No market data or other information is warranted by Reliance Capital Markets II LLC as to completeness or accuracy, express or implied, and is subject to change without notice. Any comments or statements made herein do not necessarily reflect those of Reliance Capital Markets II LLC, or their respective subsidiaries, affiliates, officers or employees. Disclaimer: Past performance is not indicative of future results. Strategic Trading Advisors is a registered DBA of Reliance Capital Markets ll LLC.

About Jody Lawrence

Jody Lawrence has been in the commodity brokerage and agriculture marketing business since 1992 and started Strategic Trading Advisors in 1999 and runs it today with his son Brady. The daily market comment his company publishes has over 7000 subscribers in 33 states and 3 countries and provides a concise overview of the world markets with ideas on farm hedging and marketing. Jody also travels the country giving 60-70 marketing meetings a year through his 22-year strategic partnership with Helena Agri-Enterprises.

About Brady Lawrence

Brady Lawrence is an Agriculture Market Specialist and Financial Advisor that focuses on commodities markets, futures and options brokerage, and helping individuals and families plan for retirement and their financial futures. Brady joined Jody at Strategic Trading Advisors in 2018 after college and supports the market research and brokerage sides of the business.